Let’s build something great

See how Totally’s API can support your reward and payout workflows. Talk to our team to explore your use case, or access our documentation when you’re ready to get started.

Book a Demo

Sending a £25 gift card to a research participant in Berlin doesn't require SWIFT routing, FX conversion, or five days of settlement. How digital reward APIs bypass traditional payment complexity for the use cases that don't require it.

.png)

Every time a business sends a reward, incentive, or recognition payout to someone in another country, the default instinct is to treat it like a financial transaction. Collect their banking details. Route the payment through SWIFT or a local bank transfer. Handle currency conversion. Manage compliance in their jurisdiction. Reconcile afterward.

For paying a vendor invoice or settling a contractor payment, that infrastructure makes sense. For sending a £25 gift card to a research participant in Berlin, a recognition reward to an employee in Dubai, or a referral incentive to a customer in Toronto, it's solving the wrong problem with the wrong tool.

Cross-border payment flows are projected to exceed $290 trillion by 2030. The average cost of sending $200 internationally still sits at 6.5%, more than double the G20's target of 3%. Settlement takes one to five business days depending on the corridor. And 12% of cross-border payments fail outright due to compliance issues, data errors, or routing problems. That infrastructure exists because moving money between bank accounts across jurisdictions is genuinely complex. But for reward and incentive payouts, most of that complexity is avoidable.

Digital gift cards and prepaid cards delivered via API bypass the traditional payment rails entirely. No banking details required from the recipient. No currency conversion for them to absorb. No SWIFT routing or intermediary fees. No multi-day settlement window. The reward is delivered via email in seconds, in the recipient's local market, with locally relevant brand options, at a cost structure that looks nothing like a cross-border wire transfer.

This piece looks at when traditional payment infrastructure is the right tool for international payouts and when it creates unnecessary complexity, how API-driven digital rewards simplify cross-border distribution for specific use cases, and what the operational and cost implications look like at scale.

The reason so many businesses default to payment infrastructure for reward distribution is that both involve sending value to someone in another country. On the surface, paying a contractor in the Philippines and sending a survey incentive to a research participant in the Philippines look like the same operational challenge. Underneath, they're fundamentally different.

Moving money means transferring funds from one bank account to another. It requires the recipient's banking details, a payment rail that connects the two institutions, currency conversion at the point of transfer, and compliance with the financial regulations governing both the sending and receiving jurisdictions. This is the right approach for contractor payments, vendor invoices, salary disbursements, and any payout where the recipient needs liquid funds in their bank account.

Delivering value means giving someone something they can use, enjoy, or spend. A gift card to a brand they choose. A prepaid Visa they can use anywhere. A multi-choice reward where they pick from a curated selection. The recipient doesn't need a bank transfer. They need a reward that arrives instantly, feels locally relevant, and creates a positive experience. The underlying mechanism is digital delivery (email, SMS, or in-app notification), not financial settlement.

When businesses use payment infrastructure for the second category, they inherit all the cost, complexity, and delay of the first category without needing any of it. Collecting banking details from thousands of research participants across 15 countries. Processing individual transfers in multiple currencies. Paying 2.5 to 3% in FX conversion fees on every transaction. Waiting one to five days for settlement while recipients wonder where their reward is. Managing tax reporting and compliance documentation in each jurisdiction manually.

For a £50 survey incentive, that overhead can represent 10 to 15% of the payout value in processing costs and administrative time, before the recipient has received anything.

API-driven digital reward delivery works on a fundamentally different model to traditional payment infrastructure.

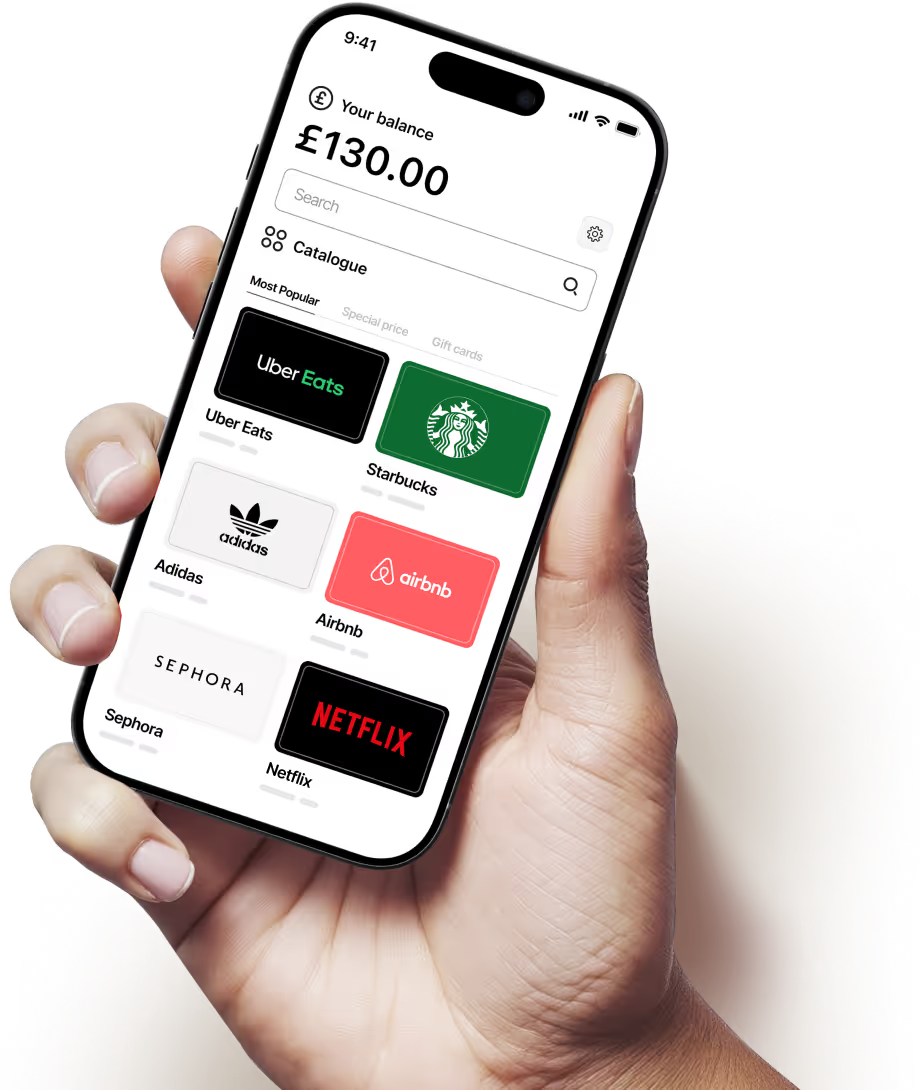

The business integrates once with the reward platform's API. When a payout is triggered (a survey is completed, a milestone is reached, a referral converts, a recognition moment occurs), the system makes a request specifying the recipient's email, the reward value, and optionally the recipient's location. The platform handles everything else: selecting locally available brands, delivering the reward in the appropriate currency, managing compliance, and tracking the transaction from issuance to redemption.

The recipient receives an email or notification within seconds containing their reward. They select from available options (or receive a specific gift card or prepaid card, depending on how the programme is configured), and the experience is complete. No banking details were collected. No currency was converted on the recipient's end. No intermediary took a cut.

For the business, the operational model is also different. Instead of managing supplier relationships and payment processing in each market, the API provides access to a single catalogue covering multiple countries. Adding a new market doesn't mean finding a new payment provider, negotiating rates, or building a new compliance process. It means the catalogue already covers that geography, and the reward programme extends there automatically.

The cost model shifts too. Traditional cross-border payments incur per-transaction fees that scale linearly with volume: more recipients means proportionally more processing cost. API-driven reward delivery operates on a platform model where the marginal cost of each additional recipient is minimal once the integration is in place. At scale, across thousands of recipients in dozens of countries, the cost difference is substantial.

Digital reward APIs aren't a replacement for payment infrastructure across all use cases. They're a better solution for a specific category of cross-border payout where the goal is delivering a branded, instant, personally relevant experience rather than settling a financial obligation.

Research incentives across multiple countries. Market research agencies running studies with participants in 10 or 20 countries face the choice between collecting banking details from every participant (slow, privacy-sensitive, operationally heavy) or sending a digital gift card via email the moment the survey is completed (instant, no banking details required, locally relevant). For a five-minute survey with a £10 incentive, the operational overhead of a bank transfer makes no sense. For a programme running thousands of incentives per month across multiple markets, the aggregate cost and time savings are significant.

Employee recognition for distributed teams. Organisations with employees across the UK, Europe, the Middle East, and Asia need a recognition programme that delivers locally relevant rewards without the HR team managing separate procurement and payment processes in each market. A single API that handles brand availability, local currency, and compliance across all territories means the recognition moment can happen instantly rather than being delayed by cross-border payment processing.

Customer rewards and marketing campaigns. Referral incentives, loyalty rewards, cashback programmes, and promotional campaigns that run across multiple markets all benefit from instant digital delivery. A customer in São Paulo who earns a referral reward should receive it in seconds with locally relevant brand options, not wait three days for a bank transfer to clear.

Gig economy and platform payouts. For platforms paying gig workers or contributors in multiple countries, digital gift cards and prepaid cards complement (and in some cases replace) traditional payment methods. Particularly for lower-value, higher-frequency payouts where the per-transaction cost of a bank transfer eats into the payout value.

The common thread across all of these is that the payout is about delivering an experience, not settling a debt. The speed, personalisation, and operational simplicity of digital reward delivery creates a better outcome for both the business and the recipient than routing the same value through traditional payment infrastructure.

Cross-border payouts of any kind involve compliance considerations, and digital rewards are no exception. The difference is in how compliance is managed.

With traditional payment infrastructure, the business is typically responsible for understanding and adhering to the tax, AML, and data protection requirements in each jurisdiction. For a company making payouts across 20 countries, that means 20 sets of rules, 20 reporting requirements, and 20 potential points of failure if something is missed.

With an API-driven reward platform, compliance can be handled at the infrastructure level. The platform applies the appropriate rules to each transaction based on the recipient's jurisdiction, the reward value, and the regulatory context, automatically. The business doesn't need to build compliance expertise in every market. The platform handles it as part of the delivery flow.

This doesn't eliminate the business's compliance obligations entirely, but it shifts the operational burden from manual, per-country management to automated, per-transaction handling. For businesses scaling their reward programmes into new markets, that shift is the difference between expansion requiring months of compliance preparation and expansion requiring a configuration change.

Value thresholds that trigger reporting obligations, tax treatment of incentives versus compensation, data protection requirements for recipient information, and AML screening all vary by jurisdiction. Getting any of these wrong carries financial and reputational risk. Having them managed within the platform infrastructure, rather than manually by an operations team that's also managing procurement and delivery, reduces that risk meaningfully.

The economics of digital reward delivery versus traditional cross-border payments look different depending on the volume, value, and use case. For the reward and incentive category specifically, the comparison tends to be favourable.

Traditional cross-border payment costs include FX conversion fees averaging 2.5 to 3% of transaction value, per-transaction processing fees that vary by corridor and method (bank transfers averaging the highest, digital wallets the lowest), intermediary fees that can strip additional value before it reaches the recipient, and the internal administrative cost of managing the payment process (collecting details, processing, reconciling, handling failures).

Digital gift card delivery costs include the wholesale cost of the gift card (typically purchased at a discount to face value), the platform fee for API access and delivery, and minimal internal administrative cost since delivery, tracking, and reconciliation are automated. There are no FX conversion fees for the recipient, no intermediary fees, no payment processing charges per transaction, and no banking detail collection or management.

For a programme delivering 5,000 incentives per month across 15 countries at an average value of £20, the aggregate cost difference between processing each one as a cross-border bank transfer versus delivering each one as a digital gift card via API is meaningful enough to change the programme economics and free budget for either more recipients or higher-value rewards.

The cost advantage becomes more pronounced at lower payout values, where the fixed costs of traditional payment processing represent a higher percentage of the transaction. A £10 survey incentive processed as a bank transfer might lose 15 to 20% of its value to fees and conversion. The same £10 delivered as a digital gift card arrives at full face value.

Totally provides the API infrastructure that businesses need to deliver digital rewards and payouts across borders without building or managing cross-border payment complexity.

That means a single API integration providing access to over 3,000 digital gift card brands across 50+ countries, prepaid Visa and Mastercard options, and multi-choice reward experiences where recipients select from locally curated options. The API handles brand availability by geography, local currency denomination, instant delivery via email, and full transaction tracking from issuance to redemption.

Compliance is managed at the platform level, with the appropriate regulatory requirements applied automatically based on the recipient's jurisdiction and the reward value. Financial reconciliation sits within the platform, giving operations and finance teams a single view of programme spend across all markets without separate reporting by country.

For businesses currently managing cross-border reward payouts through traditional payment infrastructure and finding that the cost, complexity, and delay don't match the use case, Totally provides a purpose-built alternative that's faster, simpler, and designed specifically for delivering value rather than moving money.

If your business sends reward or incentive payouts to recipients in multiple countries, a few questions will clarify whether your current infrastructure matches your actual use case.

First, look at how much of your cross-border payout volume is reward and incentive delivery versus financial settlement. If a meaningful portion falls into the first category (research incentives, recognition, customer rewards, marketing campaigns), that volume is likely better served by digital reward infrastructure than by traditional payment rails.

Second, calculate the true per-transaction cost of your current approach, including FX fees, processing charges, administrative time, and failure rates. Compare that against the cost of delivering the same value as a digital gift card. For lower-value, higher-frequency payouts especially, the gap is usually wider than expected.

Third, assess the recipient experience. How quickly do recipients currently receive their reward after earning it? How many support queries do you handle about missing or delayed payouts? How much friction is involved in claiming the reward? If the answers suggest the experience isn't matching the intent behind the programme, the delivery mechanism is likely the issue.

The businesses delivering the best cross-border reward experiences in 2026 aren't using more sophisticated payment infrastructure. They're using infrastructure designed for the specific job of delivering value to people in multiple countries, instantly, at a fraction of the cost and complexity of traditional payment rails.

Want to see how Totally can simplify your cross-border reward distribution? Drop us a note!