Let’s build something great

See how Totally’s API can support your reward and payout workflows. Talk to our team to explore your use case, or access our documentation when you’re ready to get started.

Book a Demo

This piece explores how the most effective financial platforms are using them to power cashback, drive daily engagement, and give users a reason to stay, along with the economics, compliance, and multi-market considerations behind the programmes that work.

A few years ago, digital gift cards were something a fintech might offer as a seasonal promotion or a sign-up bonus. A one-off gesture. A nice-to-have sitting at the edges of the product experience.

That's changed. Across neobanks, crypto platforms, digital wallets, and BNPL providers, gift cards have moved from the periphery of the rewards strategy to the centre of it. They're powering cashback programmes, fuelling referral loops, incentivising responsible financial behaviour, and giving crypto users a way to spend digital assets in the real world without converting to fiat. The platforms treating gift cards as infrastructure rather than incentives are seeing measurable impact on acquisition, retention, and daily engagement.

The numbers reflect the shift. The global digital gift card market reached $47.15 billion in 2025 and is projected to more than double to $98 billion by 2034. Financial services has become one of the fastest-growing segments of that market, as banks and fintechs form partnerships with gift card providers to integrate rewards directly into their apps and platforms. And from the demand side, 77% of banking customers now expect loyalty rewards, but only 45% are satisfied with what they're getting. That satisfaction gap represents a significant opportunity for platforms willing to build something better.

This piece explores how the most effective financial platforms are using digital gift cards to drive growth, and what the product, marketing, and operations teams behind those programmes are doing differently.

The shift in how financial platforms use gift cards mirrors a broader change in how these businesses think about rewards. For the first generation of neobanks and digital wallets, rewards were a marketing expense. You offered a sign-up bonus to acquire a user, maybe ran a referral campaign, and the gift card was a cost line justified by the customer it brought in.

The platforms seeing the strongest results today have moved past that model. They've recognised that gift cards serve multiple functions simultaneously when they're embedded properly into the product.

They're a redemption layer for loyalty and cashback. When a user earns cashback or loyalty points, they need somewhere to spend them. Gift cards provide a broad, flexible redemption catalogue that gives users genuine choice without the platform needing to build relationships with thousands of individual retailers. And there's a meaningful economic advantage: platforms can often purchase gift cards at a discount to face value, meaning a user redeeming £5 of points on a coffee voucher might only cost the platform £3.50 to £4. That margin difference, compared to straight cash rebates, makes loyalty programmes significantly more sustainable at scale.

They drive daily engagement. Financial apps compete for attention in a crowded home screen. Platforms that surface personalised gift card offers, rotating discounts, or category-specific rewards within the app give users a reason to open it beyond checking their balance. When your banking app is also where you browse discounted gift cards or redeem this week's cashback, the engagement loop tightens.

They enable crypto-to-real-world spending. For crypto platforms and crypto-backed neobanks, gift cards solve a specific and valuable problem: they allow users to spend digital assets at everyday retailers without the friction of converting to fiat currency first. A user holding Bitcoin or stablecoins can purchase a gift card from within the platform and use it at a high street shop, a food delivery service, or an online retailer. That bridge between digital assets and real-world spending is one of the most practical use cases for gift cards in the fintech space.

They support onboarding and activation. A well-chosen gift card as a welcome reward doesn't just incentivise sign-up. It creates the first moment of value in the product experience. When a new user receives a reward they actually want within their first session, it establishes a pattern of engagement that increases the likelihood of them becoming an active, retained user rather than a sign-up who never returns.

Across the neobanks, fintechs, and digital wallets running effective gift card programmes, a few patterns consistently show up in how they design and deliver the experience.

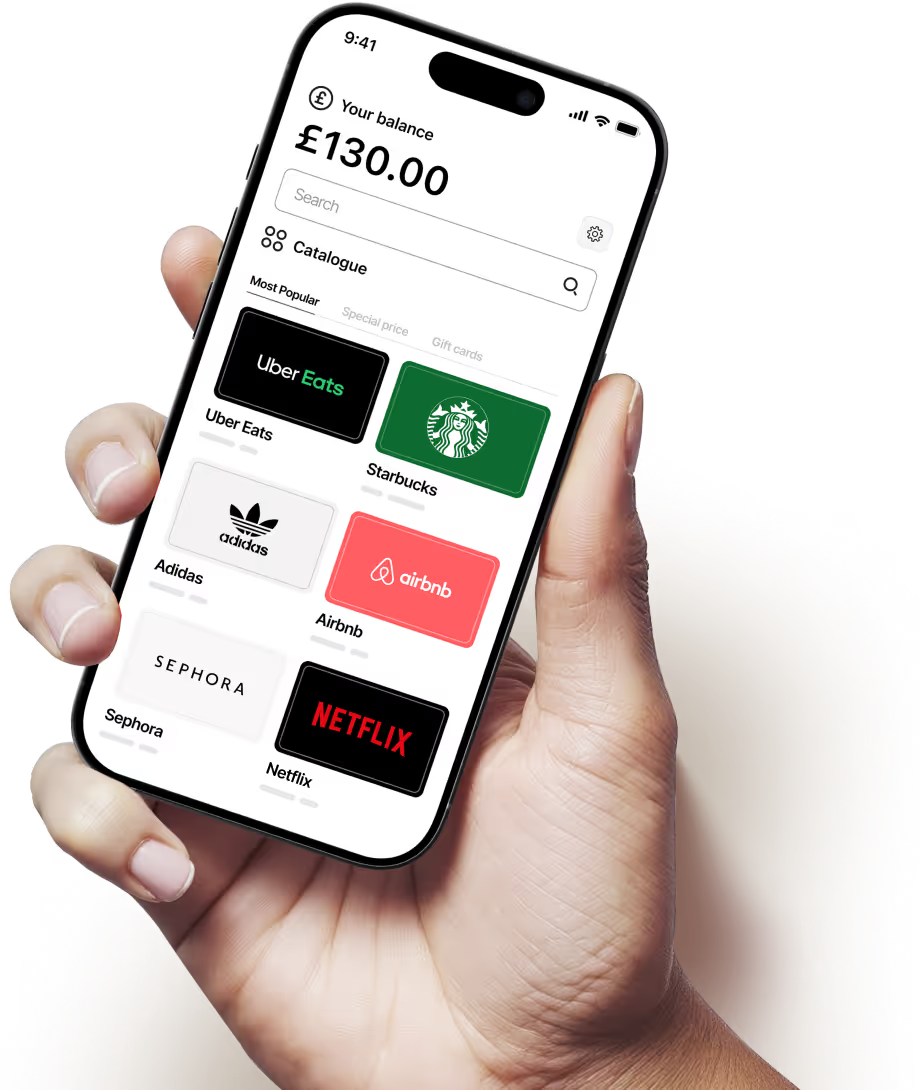

The gift card experience lives inside the product, not outside it. The platforms getting the best results don't link users out to a third-party gift card page. The browsing, selection, and redemption happen within the app itself, branded and designed to feel native. The user never leaves the product environment, which means the gift card interaction reinforces the platform's brand rather than handing that moment to someone else. This is the single biggest differentiator between programmes that drive engagement and programmes that feel like an afterthought.

Selection is curated, not exhaustive. Having access to thousands of brands is valuable at the infrastructure level, but what the user sees should be curated and relevant. The strongest programmes surface a manageable selection of gift card brands tailored to the user's location, spending patterns, and preferences, then allow them to explore further if they want to. A UK user sees Pret, Deliveroo, and M&S first. A user in the Gulf sees brands that are locally relevant and culturally appropriate such as Careem, Talabat, and Carrefour. The platform's transaction data makes this kind of curation possible, and when it's done well, it makes the gift card experience feel considered rather than generic.

Rewards are tied to specific behaviours, not just tenure. The most effective programmes connect gift card rewards to actions the platform wants to encourage: completing onboarding steps, setting up direct deposit, making a first transaction, referring a friend, reaching a savings milestone, or (in the BNPL context) making payments on time. Tying rewards to behaviour creates a feedback loop where the gift card incentivises the action that drives the business metric the platform cares about.

Delivery is instant. In a world where financial platforms process transactions in seconds, a reward that takes 24 to 48 hours to arrive feels broken. Instant delivery, the gift card appears in the user's account the moment they earn or redeem it, is fundamental to the experience working. Delays break the connection between the action and the reward, reducing both the satisfaction and the behavioural reinforcement.

The programme compounds rather than depletes. A one-off sign-up bonus is a cost. A programme that rewards ongoing engagement, where the reward value increases with loyalty tier or usage frequency, creates a compounding incentive for users to stay and deepen their relationship with the platform. The most sophisticated programmes layer gift card rewards into a broader loyalty architecture where earning and redeeming becomes part of the regular product experience.

Understanding why gift cards have become the preferred reward format for financial platforms requires looking at the economics compared to the alternatives.

Cost advantage over cash rebates. Cash back is simple for the user but expensive for the platform. Every pound of cashback costs the platform a pound (plus processing). Gift cards, purchased at wholesale rates, typically cost 5 to 30% less than face value depending on the brand and volume. A platform offering £10 of "cashback" in the form of a gift card might pay £7 to £9 for it. At scale, across millions of redemptions, that margin difference is substantial.

Traceable and compliant. Unlike cash payments, gift cards create a clear audit trail: what was issued, to whom, when, and at what value. For financial platforms operating under regulatory scrutiny, this traceability is valuable for compliance, reporting, and fraud prevention. Every transaction is documented in a way that cash or points-based systems don't always achieve as cleanly.

Low operational overhead when API-driven. When gift card issuance and delivery are handled through an API integration rather than manual processes, the operational cost per reward is minimal. The platform triggers the reward through an automated event (user completed onboarding, referral converted, cashback threshold reached) and the gift card is issued and delivered without anyone on the operations team touching it. This is what allows programmes to scale from hundreds to millions of users without adding headcount.

User satisfaction and perceived value. 78% of neobank users globally are millennials or Gen Z, demographics that index heavily toward digital gift cards as a preferred reward format. They're familiar, trusted, and immediately useful. A £10 coffee voucher or food delivery credit feels more tangible and exciting than £10 appearing as a line item on a bank statement, even though the monetary value is identical.

Financial platforms that operate across borders face a specific challenge with gift card programmes: relevance needs to be local while infrastructure needs to be global.

A neobank serving users in the UK, Europe, and the Middle East can't offer the same gift card catalogue in every market and expect it to land well. Brand preferences, spending habits, and even the categories that feel appropriate as rewards vary significantly by geography.

The platforms handling this well tend to work with a single gift card infrastructure provider that maintains a broad, multi-country catalogue, and then apply their own curation layer on top. The infrastructure handles the complexity of brand availability, local currency, and compliance across jurisdictions, while the platform's product team controls what the user actually sees and how it's presented within the app.

This separation of infrastructure and experience is important because it allows the product team to move quickly. Launching a gift card programme in a new market becomes a configuration task rather than a procurement project. New brands can be added, removed, or repositioned without engineering work. And the programme can adapt to local events, seasons, and cultural moments without rebuilding anything from scratch.

For crypto platforms specifically, the cross-border question has an added layer. Crypto-to-gift-card conversion needs to handle exchange rate volatility, settlement timing, and the regulatory treatment of digital assets in each market. Getting this right requires infrastructure that's been built with these complexities in mind, not a generic gift card API that was designed for a simpler use case.

Financial platforms operate in one of the most heavily regulated environments in business. Any reward programme needs to work within the platform's existing compliance framework, not create new risk.

Gift cards sit in a useful space here because they're a well-understood instrument from a regulatory perspective. They have established treatment under anti-money-laundering rules, tax reporting requirements, and consumer protection frameworks across most major jurisdictions. Compared to novel reward formats like tokens or crypto-based incentives, gift cards carry less regulatory ambiguity.

That said, the compliance requirements do vary by market and the details matter. Value thresholds that trigger reporting obligations differ by jurisdiction. Cross-border issuance introduces questions about which market's rules apply. And platforms operating under specific financial licences may have restrictions on the types of incentives they can offer and how they're classified.

The practical implication is that any gift card infrastructure provider serving financial platforms needs to handle compliance at the transactional level, automatically applying the right rules to each issuance based on the recipient's jurisdiction, the card value, and the platform's regulatory context. Platforms that try to manage this manually or through workarounds end up creating compliance debt that becomes increasingly difficult to unwind as the programme scales.

Totally provides the reward infrastructure that financial platforms need to run gift card programmes at scale, from early-stage neobanks launching their first referral campaign to established platforms managing multi-country loyalty ecosystems.

That means API-driven access to over 3,000 digital gift card brands across 50+ countries, alongside prepaid Visa and Mastercard options. The API handles gift card sourcing, issuance, delivery, and reconciliation, so the platform's engineering team integrates once and the programme scales from there. Rewards can be triggered by any event in the platform's system: sign-up, referral, transaction milestone, cashback threshold, or any custom trigger the product team defines.

For crypto platforms and crypto-backed neobanks, Totally's infrastructure supports the bridge between digital assets and real-world spending, enabling users to convert balances into gift cards that can be used at everyday retailers.

Every gift card touchpoint is fully brandable, so the experience looks and feels native to the platform rather than handing the user off to a third party. Real-time tracking provides visibility into redemption rates, popular brands, and programme costs, giving product and finance teams the data they need to optimise the programme over time.

If you're running a financial platform and you're either building a gift card programme for the first time or looking to improve what you've already got, a few starting points will help focus the effort.

First, define what behaviour you're trying to drive. Acquisition, activation, engagement, retention, and referral all require different programme designs with different reward triggers and different success metrics. Trying to do everything at once usually means doing none of it well.

Second, evaluate your current infrastructure. Can your system trigger a gift card issuance in real time based on a user event? Can it handle multiple markets and currencies? Is the experience branded and native to your app, or does it hand users off to a third-party interface? The answers to these questions determine whether you need a new infrastructure partner or whether you can build on what's already in place.

Third, start measuring the economics properly. Track the cost per reward against the lifetime value of the users that reward helps you acquire or retain. Compare gift card programme costs against the cost of equivalent cash rebates. Model the margin advantage at your current scale and at the scale you're planning for. The business case for gift cards over cash tends to get stronger as the programme grows.

Want to explore how Totally's gift card infrastructure can power your platform's growth? Drop us a note!

.avif)