Let’s build something great

See how Totally’s API can support your reward and payout workflows. Talk to our team to explore your use case, or access our documentation when you’re ready to get started.

Book a Demo

Fintech retention sits at just 37%. How embedded reward programmes create the structural loyalty that sign-up promotions can't.

Fintechs have become very good at getting people through the door. Cashback offers, fee-free introductory periods, referral bonuses, and sign-up rewards have driven user growth across neobanks, digital wallets, and payment platforms at a pace traditional banking has struggled to match. 78% of neobank users globally are millennials or Gen Z, a demographic that responds strongly to incentive-led acquisition.

Strong acquisition numbers, until retention falls through the floor. Fintech retention sits at just 37%, the lowest of any industry measured. Digital banking churn runs between 15% and 25% annually. 39% of users maintain accounts with more than two neobanks simultaneously, which means they're hedging rather than committing. And customer acquisition costs across digital banking platforms rose 22% between 2022 and 2024, which makes every churned user progressively more expensive to replace.

The promotional offers that drove initial growth are now table stakes. Every competitor offers cashback. Every neobank has a referral programme. Every digital wallet waives fees for the first few months. When everyone is offering the same thing, none of it creates differentiation, and none of it builds the level of brand loyalty that keeps someone from switching when the next offer arrives.

The fintechs focusing on customer loyalty are the ones winning at the moment. They're moving digital rewards from just being a line item on their marketing budget, into the actual product experience itself. They’re embedding rewards into the everyday financial journey rather than bolting them on as a one-off acquisition tactic.

The disconnect between sign-up growth and long-term retention makes more sense when you look at what acquisition offers actually achieve psychologically.

A sign-up bonus creates a transactional relationship from the first interaction. The customer receives value in exchange for opening an account. Once the bonus is claimed, the transaction is complete. There's no ongoing reason to stay beyond the product itself, and if a competitor's product is functionally similar (which in fintech, it often is), the next sign-up offer becomes a reason to move.

Increasing retention by just 5% can boost profitability by up to 95%, which means the economics of solving this are significant. 65% of revenue for most businesses comes from existing customers rather than new ones. For fintechs spending heavily on acquisition, every point of retention improvement changes the unit economics meaningfully.

The shift required is from rewarding the act of signing up to rewarding the behaviours that indicate genuine engagement: regular usage, savings milestones, responsible spending, payment consistency, referrals, and deeper product adoption. When rewards are tied to ongoing behaviour rather than a one-time action, they create a continuous incentive structure that makes staying progressively more valuable than leaving.

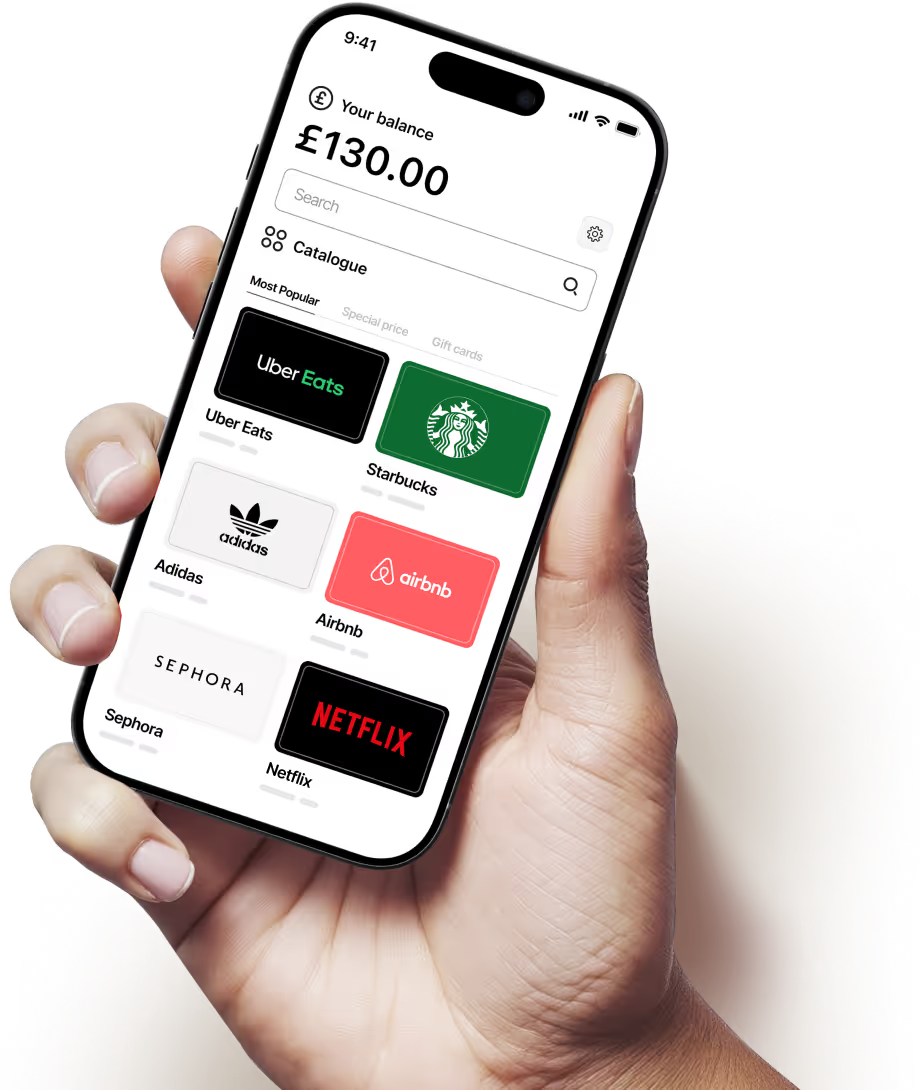

68% of consumers consider gift cards the most attractive form of reward or incentive across all demographics. For fintechs specifically, digital gift cards address several challenges that other reward formats struggle with.

They connect the fintech experience to brands people already love. A neobank's own ecosystem, no matter how well designed, is limited in the experiences it can offer. Digital gift cards extend the reward moment into the broader world of retail, dining, entertainment, and services that users engage with daily. When someone earns a reward through their banking app and redeems it at their favourite coffee shop or streaming service, the positive association transfers back to the platform that gave it to them.

They work within the product experience. The strongest fintech loyalty programmes don't send users to a separate website to claim their reward. The browsing, selection, and redemption happen within the app itself. The user never leaves the platform environment. For Gen Z users, who are 2.5 times more likely to demand a fast, seamless purchasing journey, this in-app experience is a baseline expectation rather than a differentiator.

They support multiple loyalty mechanics simultaneously. Cashback can be redeemed as gift cards (at a lower cost to the platform than cash equivalents). Milestone rewards for savings targets or spending streaks can be delivered as curated gift card selections. Referral bonuses can arrive instantly as a multi-choice reward. The format is flexible enough to serve across the full customer lifecycle rather than being limited to a single use case.

They create the emotional response that cash equivalents don't. A £10 statement credit gets absorbed into the account balance and forgotten. A £10 gift card to a brand someone loves creates a distinct moment of pleasure. The brain categorises it differently, filing it under "treat" rather than "income," which makes the experience more memorable and more likely to drive the positive brand association that retention depends on.

The fintechs seeing the strongest retention aren't running loyalty as a standalone programme. They're embedding reward mechanics into the core product in a way that makes engagement progressively more valuable over time.

Reward ongoing usage. Points or rewards that accumulate with regular transactions, bill payments, or savings deposits create a continuous incentive to keep the account active. When a user has accumulated value within the platform, switching to a competitor means walking away from that accumulated progress.

Introduce milestone-based rewards at the moments where churn risk is highest. The first 90 days are critical for fintech retention. A reward delivered at the 30-day mark for completing onboarding steps, another at 60 days for reaching a usage threshold, and a third at 90 days for sustained engagement creates three intervention points during the period where most churn occurs.

Use transaction data to personalise the reward experience. Fintechs have rich first-party data on how their users spend. Someone who regularly spends at restaurants should see dining brands surfaced first in their reward catalogue. Someone who spends on fitness and wellness should see relevant brands in that category. This personalisation signals that the platform understands the user as an individual, not just an account number.

Make the programme visible and progressively rewarding. A loyalty tier that unlocks better rewards with continued engagement creates a psychological commitment to the platform. The user has "earned" their status and is less likely to abandon it. Tiered structures work particularly well for fintechs because they can be tied to tangible product benefits (better rates, higher limits, premium features) alongside the reward component.

For fintech product and operations teams, the practicality of how rewards are delivered matters as much as the strategy behind them.

Cash-based rewards require payment processing, tax handling, and reconciliation for every transaction. At the volumes fintechs operate at, this creates significant operational overhead. Digital gift cards, delivered through an API integration, can be issued instantly, tracked automatically, and reconciled within the reward platform without manual intervention.

For fintechs operating across multiple markets, the ability to deliver locally relevant rewards in local currency from a single infrastructure provider removes a layer of complexity that would otherwise require separate supplier relationships in each country.

And because every gift card interaction is tracked (issuance, delivery, redemption, value, brand selected), the data generated feeds directly into the personalisation and optimisation of the programme over time. Each cycle of rewards creates better data, which creates better targeting, which creates better engagement, which creates better retention.

Totally provides the reward infrastructure that fintechs, neobanks, and digital wallet providers need to embed personalised, branded loyalty experiences directly into their product.

That means API-driven access to over 3,000 digital gift card brands across 50+ countries, prepaid Visa and Mastercard options, and multi-choice reward experiences where users select from a curated catalogue. The API integrates into existing fintech platforms, enabling automated reward delivery triggered by transaction milestones, onboarding completion, referral conversion, or any custom event the product team defines.

Every reward touchpoint is fully brandable, so the experience feels native to the fintech platform rather than handing the user off to a third party. Real-time tracking gives product and growth teams visibility into redemption patterns, popular brands, and programme costs, providing the data needed to optimise the loyalty experience continuously.

For fintechs where the difference between a retained user and a churned one compounds across millions of accounts, Totally provides the infrastructure to make loyalty operational at scale.

If your fintech is experiencing strong acquisition but struggling with retention beyond the introductory period, the loyalty gap is likely structural rather than promotional.

First, map where your churn concentrates. If the first 90 days account for the majority of losses, that's where the first reward interventions should go. Milestone rewards at 30, 60, and 90 days tied to engagement behaviours create structural reasons to stay through the critical early period.

Second, evaluate whether your current rewards are creating ongoing value or one-off transactions. If the only incentive in your programme is the sign-up bonus, everything after that moment is unassisted retention. Layering in usage-based rewards, personalised gift card offers, and progressive loyalty tiers creates continuous engagement rather than a single acquisition spike followed by silence.

Third, look at what your transaction data already tells you about your users and how much of that knowledge currently shapes the reward experience. For most fintechs, the answer reveals a significant gap between available data and how it's being used to personalise loyalty. Closing that gap is where the biggest retention gains tend to sit.

The fintechs that will hold onto their users over the next two to three years won't be the ones with the biggest sign-up bonuses. They'll be the ones where the experience of staying gets better every month.

Want to see how Totally can power your fintech loyalty programme? Drop us a note!

.avif)